The IRS appears to have removed the Delinquent FBAR Submission Procedures as of June 30, 2026.

A major change for U.S. taxpayers abroad with late FBARs

This was a shock to taxpayers and tax professionals. The procedure disappeared without a clear IRS announcement, transition guidance, or explanation of what should happen next for taxpayers with late FBARs.

For years, this procedure was the common path for taxpayers who had missed FBAR filings but had otherwise properly reported their foreign income on their U.S. tax returns. It gave many taxpayers a clear way to catch up on FBARs without entering the full Streamlined Filing Compliance Procedures.

That program appears to be gone.

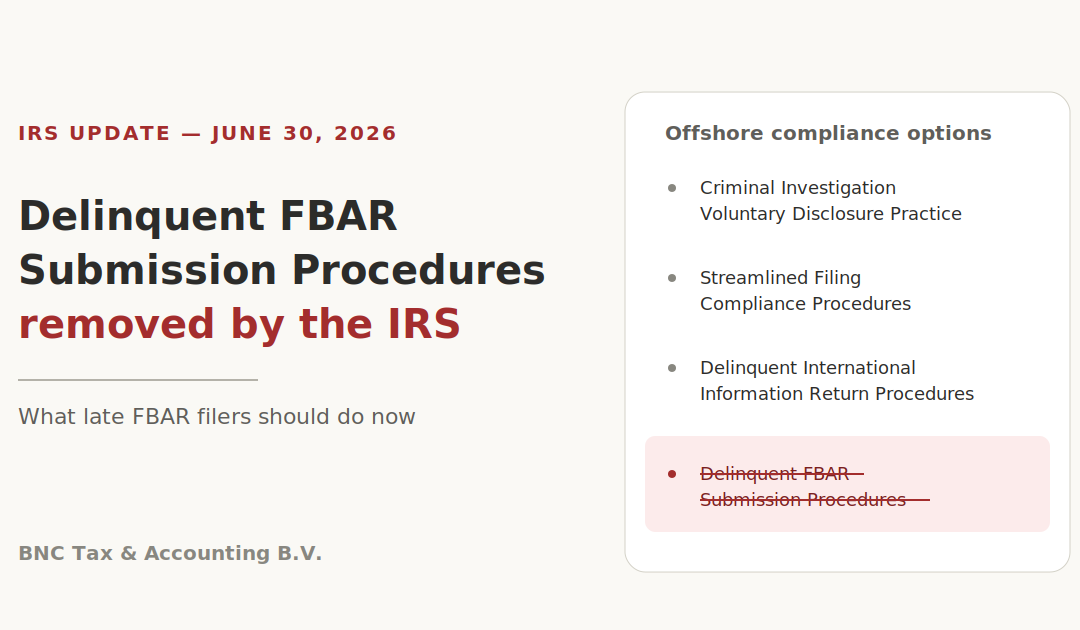

The current IRS page for “Options available for U.S. taxpayers with undisclosed foreign financial assets” now lists only three offshore compliance options:

- IRS Criminal Investigation Voluntary Disclosure Practice

- Streamlined Filing Compliance Procedures

- Delinquent International Information Return Submission Procedures

The Delinquent FBAR Submission Procedures are no longer listed.

So what does this mean if you just discovered that you missed FBARs?

The short answer: do not panic. It is time to evaluate your options.

What is an FBAR?

The FBAR, officially FinCEN Form 114, is used to report foreign financial accounts when a U.S. person has more than $10,000 in total foreign account value at any point during the year.

This can include:

- Foreign checking and savings accounts

- Investment accounts

- Certain pension or retirement accounts

- Business accounts

- Joint accounts

- Accounts where you have signature authority

The FBAR is not filed with your tax return. It is filed separately through FinCEN’s BSA E-Filing System.

Many U.S. citizens abroad miss this filing because they assume local bank accounts in the country where they live are not “foreign” to them. For U.S. reporting purposes, they are.

What changed after June 30, 2026?

Before June 30, 2026, many taxpayers with FBAR-only delinquency could use the Delinquent FBAR Submission Procedures.

That procedure was generally used when:

- The taxpayer missed one or more FBARs;

- All income from the foreign accounts was reported on the U.S. tax return;

- All U.S. tax was paid;

- The IRS had not already contacted the taxpayer;

- The taxpayer was not under civil or criminal investigation.

The key benefit was penalty comfort. Under the old procedure, the IRS stated that it would not impose a penalty if the taxpayer met the conditions.

Now that this procedure appears to have been removed, taxpayers no longer have the same clear IRS-published penalty-free path for FBAR-only mistakes.

That is the real change.

It does not mean every late FBAR will be penalized.

It does not mean every taxpayer must use Streamlined.

It does mean the filing strategy now requires a more careful review.

Can taxpayers still file late FBARs?

Yes.

The IRS’s current FBAR guidance still says that if the IRS has not contacted the taxpayer about a late FBAR and the taxpayer is not under civil or criminal investigation, the taxpayer should file late FBARs as soon as possible to keep potential penalties to a minimum.

However, the IRS also says that filing an FBAR late, or not filing at all, is a violation and may subject the taxpayer to penalties.

That means a direct late FBAR filing may still be possible, but it no longer comes with the same published no-penalty assurance that existed under the Delinquent FBAR Submission Procedures.

This is why taxpayers should not treat late FBAR filing as a simple administrative cleanup.

Should every late FBAR now go through Streamlined?

No.

This is the most important point.

The removal of the Delinquent FBAR Submission Procedures does not automatically mean that every taxpayer with late FBARs should use the Streamlined Filing Compliance Procedures.

Streamlined is broader than FBAR filing. It is designed for taxpayers whose failure to report foreign financial assets, pay tax, and file required information returns was non-willful.

The IRS requires taxpayers using Streamlined to certify that their conduct was non-willful. The IRS defines non-willful conduct as conduct due to negligence, inadvertence, mistake, or a good faith misunderstanding of the law.

For many U.S. taxpayers abroad, Streamlined can be the right path.

But it is not always the right path.

When might Streamlined be the right option?

Streamlined may be appropriate when the late FBAR issue is part of a broader U.S. tax compliance problem.

This may include:

- Unfiled U.S. tax returns

- Unreported foreign interest, dividends, capital gains, pension income, rental income, or business income

- Missed Form 8938

- Missed Forms 5471, 8858, 8865, 3520, 3520-A, or 8621

- Foreign business ownership

- Foreign pension or investment reporting issues

- Multiple years of incomplete U.S. international tax reporting

For U.S. taxpayers living outside the United States, the Streamlined Foreign Offshore Procedures often provide a practical way to correct several years of tax returns, FBARs, and international reporting forms in one package.

For eligible foreign-resident taxpayers, Streamlined Foreign generally requires three years of tax returns and six years of FBARs. If completed properly, eligible taxpayers are not subject to FBAR penalties, information return penalties, accuracy-related penalties, failure-to-file penalties, or failure-to-pay penalties, unless the IRS later determines fraud or willfulness.

That is why Streamlined can be powerful. But it must be used correctly.

When might direct late FBAR filing still make sense?

A direct late FBAR filing may still be reasonable when the issue is truly limited to FBARs.

For example, this may apply when:

- U.S. tax returns were filed;

- All foreign income was reported;

- All U.S. tax was paid;

- No Form 8938 or other international form was missed;

- The accounts were ordinary local bank accounts;

- The taxpayer was not contacted by the IRS;

- The taxpayer has a credible reasonable cause explanation.

In this type of case, a taxpayer may still file late FBARs through FinCEN and include a late-filing explanation.

But this should be reviewed carefully first. The old penalty-free procedure appears to be gone, and the explanation matters.

Will all late FBARs be penalized now?

No.

The IRS says FBAR penalty assertion depends on the facts and circumstances. A late FBAR is not automatically penalty-free, but it is also not automatically penalized.

The facts matter.

A taxpayer who lives abroad, uses ordinary local bank accounts, reported all income, and corrects the issue voluntarily is in a very different position from a taxpayer who hid accounts, failed to report income, ignored prior advice, or is already under IRS contact.

That is why the first step should be a compliance review, not a rushed filing.

What should you do if you missed FBARs?

If you missed FBARs, the most important question is not simply “How do I file them?”

The better question is:

Which compliance path is safest for my facts?

Before filing, taxpayers should review:

- Which years are late;

- Whether all U.S. tax returns were filed;

- Whether all foreign income was reported;

- Whether Form 8938 or other international forms were required;

- Whether the taxpayer qualifies for Streamlined Foreign or Streamlined Domestic;

- Whether there are any facts that could raise willfulness concerns;

- Whether a direct late FBAR filing with reasonable cause may be appropriate.

This is exactly the type of situation where professional review matters.

Bottom line

The IRS appears to have removed the Delinquent FBAR Submission Procedures without warning as of June 30, 2026.

That is a major change for U.S. taxpayers abroad.

The right path is dependent on the facts. It may be a direct late FBAR filing. It may be Streamlined Foreign Offshore. It may be Streamlined Domestic Offshore. In higher-risk cases, it may require a more cautious legal review.

Need help with late FBARs after the IRS removed the delinquent FBAR procedure?

If you recently discovered missed FBARs, BNC Tax & Accounting can help you review your late FBARs, determine whether you qualify for the Streamlined Filing Compliance Procedures, and decide which filing path best fits your situation.

This rule change happened quickly, and the IRS has not provided much explanation. Before filing late FBARs, get a professional review so you understand your options and your risk.

Contact BNC Tax & Accounting to schedule a late FBAR and Streamlined eligibility review.

Discover Expert Tax Solutions

Unlock the potential of your life abroad with a personalized US tax consultation.

Christie DuChateau, EA – Owner & Tax Advisor

Christie DuChateau, EA – Owner & Tax Advisor

Christie specializes in complex tax issues for Americans living abroad, drawing on her own decade of experience as an expat to understand the unique challenges her clients face.